Balanced Scorecard: A tool for effective strategy implementation

From the initial vision to the concrete strategy and lastly to tangible success. How can you monitor whether the business strategy is actually working? Two business experts, Robert S. Kaplan and David P. Norton, devised a tool for making the strategy more successful. In the 1990s, they developed a system for improving controlling within companies: the balanced scorecard (BSC). Thanks to its clear presentation of cause and effect, decision-makers have a tool that they can use to manage their companies more effectively.

Balanced scorecard: definition and how it works

The balanced scorecard involves the interaction of cause and effect: whatever you put into a system also determines to some extent what you get out. Moreover, changes in one area can have consequences in completely different areas – both positively or negatively. The BSC is there to visualize and measure these kinds of changes.

To use a balanced scorecard, it is first necessary to formulate a vision and a strategy, then define critical success factors (CSFs) on this basis. These key indicators show how successfully the strategy is being implemented, with the main characteristic of this system being that they do not necessarily have to be monetary. In other words, they do not merely relate to returns and revenue figures, but they can also express the number of new customers and the associated cause-and-effect chains, for instance.

Perspectives of the company

When analyzing the company and business strategy using a balanced scorecard, four different perspectives are considered. These reflect the business areas that are critical for the success of the company and help create a comprehensive picture of the company. These four areas are as follows:

Finance perspective

This perspective is primarily adopted to consider the monetary values in the company. They allow the economic consequences of the strategy to be understood. Revenue and profitability play a critical role here – i.e. key indicators that directly tie in with the continued existence of the company. This perspective also takes investors and shareholders into consideration, which is why it is also important to include key indicators that are relevant for these two groups when analyzing the company from this perspective. For instance, the return on investment (ROI) is particularly important for investors.

Customer perspective

The customer perspective concerns how consumers view the company. For them, the most interesting factors are not the same as those for investors: it makes sense to examine key indicators on customer satisfaction, for example. The proportion of new customers is also a useful value to measure from this perspective, as is the end price of the products offered.

Process perspective

The process perspective refers to an internal look at the company’s processes. This perspective is used to assess and improve internal workflows. Key indicators that are of interest when analyzing from this perspective include the costs of working processes, as well as the adherence of processes to deadlines. Quality controls can also be relevant from the process perspective.

Learning and growth perspective

The learning and growth perspective helps evaluate the potential for further development. Here, the balanced scorecard shows, for example, that the employees and their qualities play a substantial role in the successful implementation of strategies. Key indicators from personnel development in particular are important in this context. For example, the level of qualification of employees and the fluctuation rate within the company are significant factors from the learning and growth perspective. Besides the employees, the development of products and services also influences the success of the company.

These four perspectives are suitable for the structure of many, but not all, companies, so it can be useful to replace or add one or more areas to the balanced scorecard. For some companies, for instance, the supplier or communication perspective may be important.

Balance of Areas

The name “balanced scorecard” already suggests an important characteristic for the successful implementation of business strategies: the right balance. So far, we have only considered one aspect of the scorecard: the measurement of values within selected perspectives. However, the perspectives are not chosen in an arbitrary manner. Instead, they need to be balanced to enable as complete an evaluation as possible. Analysis using a balanced scorecard is intended to prevent an excessively one-sided assessment of the company’s performance – for instance, by only considering returns. Experience has shown that such a restricted view only has limited benefits. In many cases, financial aspects alone do not appropriately reflect the success of business strategies.

Besides, simply measuring key indicators is not enough to make a strategy successful. The balanced scorecard method provides management information on aspects that require work in future and on which changes are necessary in order for a suitably adjusted strategy to move the company forwards. Balance therefore not only plays a role in assessing the company but also in its development. To prevent the development of the company from only progressing within a small area, it is important to not only define multiple perspectives but also formulate goals from the different perspectives. This ensures that an actual measured value is always accompanied by a target value. If it becomes clear that a goal will not be achieved in a certain area, swift action can be taken, avoiding a situation in which individual business areas remain underdeveloped.

Apart from the goals, responsibilities must also be defined. Especially in larger companies, it is almost impossible for a single person to manage the entire business and take care of all business areas; it is therefore necessary to define who is responsible for ensuring the business goals are achieved in each of the areas.

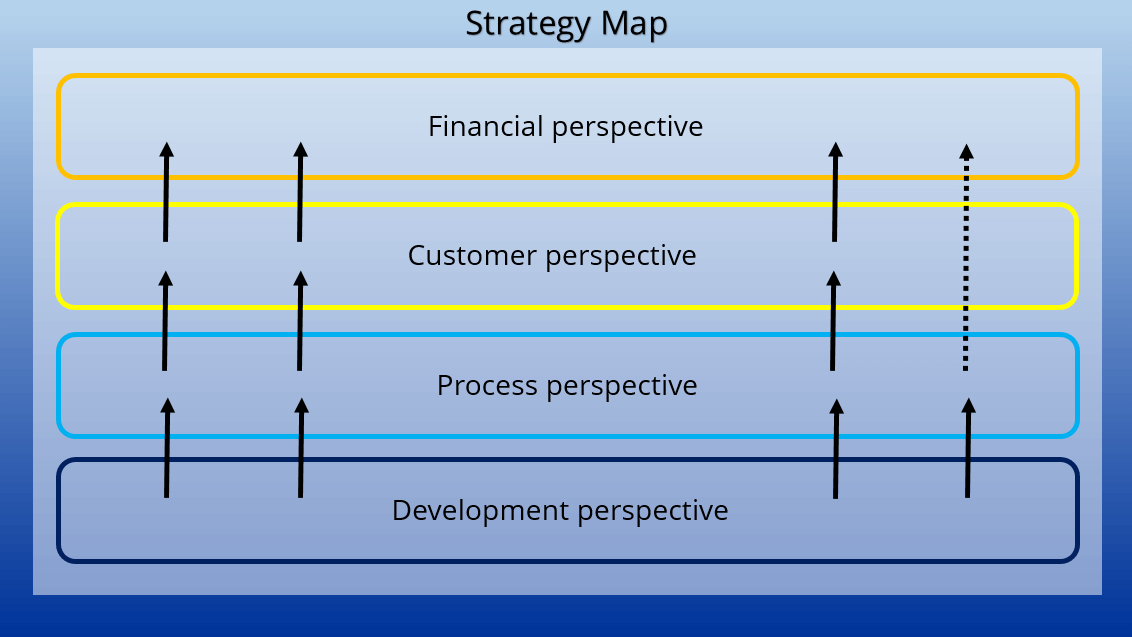

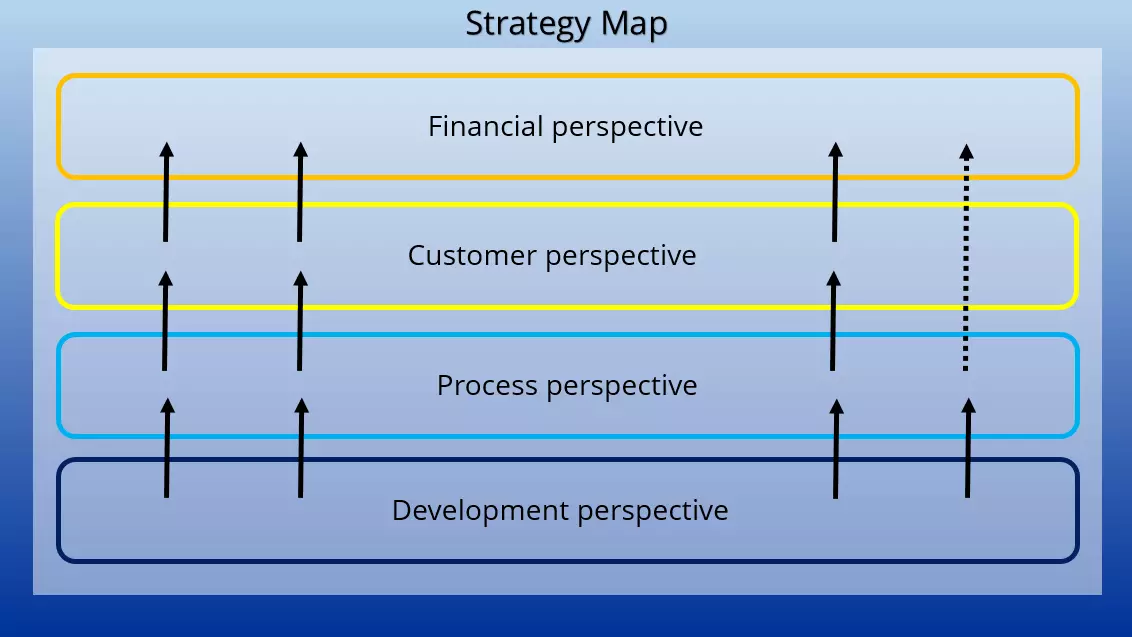

Cause and effect: the strategy map

The balanced scorecard is based on the principle of cause and effect. Developments in one area typically also have significant effects on the key indicators in other areas. This principle can be illustrated using a strategy map, which shows how the achievement of goals in a perspective area influences the other perspectives. A sequence can also be determined. The qualification of employees and the level of development of the company (development perspective) directly impact how efficiently products and services can be delivered (process perspective). This, in turn, affects the satisfaction of customers and the price (customer perspective). Furthermore, the customers purchase the products and thereby generate revenue and returns (financial perspective).

The strategy map can help companies to formulate their business strategy. For example, a certain level of revenue can be defined as an overarching goal. The question is then how it can be achieved. One possibility would be to increase the number of new customers. As the next step, it is necessary to think about how these new customers are to be acquired. This leads to a new goal in the process perspective. Finally, the requirements (and hence goals) that are necessary from a development perspective in order to achieve the target value of the process perspective also need to be identified. The strategy map is thus created using a top-down approach.

There is no reason to use only one strategy map and one balanced scorecard within a company. In practice, a balanced scorecard is typically created for each company level, for each team or each region, which in turn depends on a superordinate level. This results in a layered structure.

What are the advantages of the BSC?

The balanced scorecard serves multiple purposes at the same time: It first forces business owners to formulate clear visions and strategies. Secondly, key indicators have to be defined that are critical for implementing the respective strategy. This makes the complexity of a company perceptible and, above all, also transparent for all employees. Using a balanced scorecard can therefore be helpful first and foremost in the development and common understanding of a strategy.

By setting key indicators, the balanced scorecard also makes the success of implemented strategies measurable (and hence also the success of the company itself to a certain degree). To take these measurements, the company is observed extensively from all sides and at least four different perspectives in order to assess its strategy much more comprehensively than would be the case with a sole focus on revenue.

In order to truly exhaust the benefits of the balanced scorecard, it is important to avoid the mistake of viewing the BSC as merely collecting key indicators, which are already gathered anyway when controlling. Instead, it is important to consider the key indicators in relation to the business strategy and to maintain an overview of the interactions between the individual business areas. If revenues do not match expectations, for example, it can certainly be useful to adopt the process perspective to examine whether there are factors for increasing revenue in this area.

The inventors of the balanced scorecard, Kaplan and Norton, pointed out the risk that the BSC may be used incorrectly and only considered as a collection of isolated key values. However, it is the combination of strategy, goals, and measurement values that is essential for successfully applying balanced scorecards.

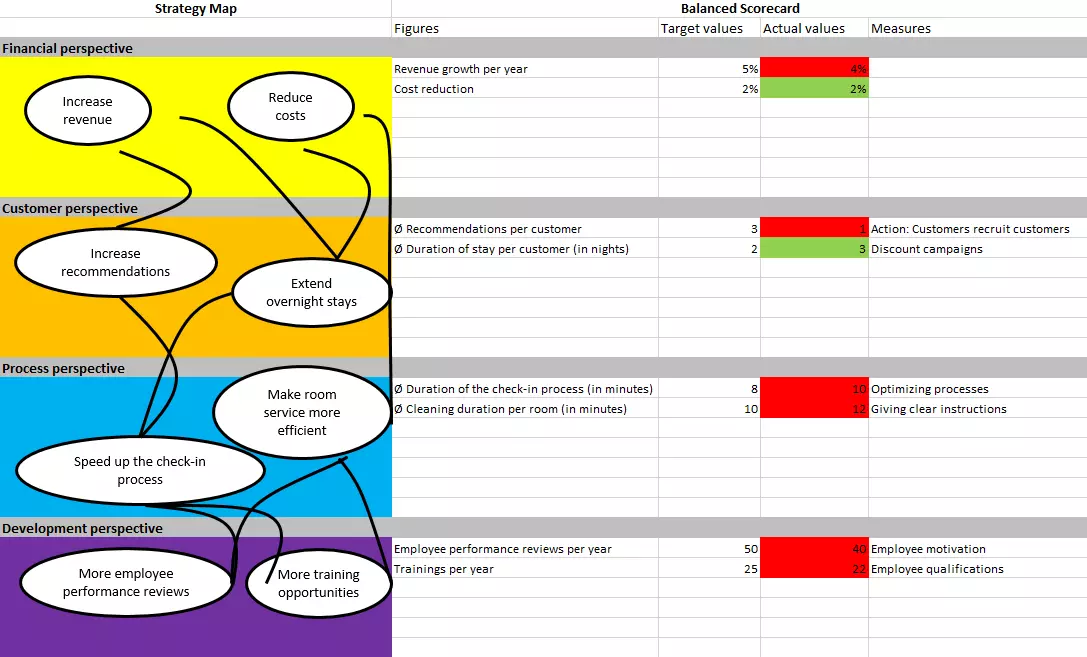

Structure of the balanced scorecard explained using an example

Imagine a large hotel would like to introduce a balanced scorecard in order to manage its business more effectively. The company first needs to develop a strategy and visualize it in a strategy map. As its top goal, the company wishes to increase revenues. To achieve this goal, more overnight stays have to be generated. The hotel intends to increase the number of recommendations per customer. However, for customers to be prepared to recommend the hotel, they need to be impressed by a very high level of service. The hotel decides to measure the rate at which people check in as a key indicator. In order to reduce processing times and improve service, employees must first be trained and staff meetings conducted. The number of these training sessions and staff meetings can also be collected. An example below shows what a balanced scorecard might look like for these key indicators.

Are you looking for even more tools that you can use to manage your business successfully? Both the BCG Matrix and the Ansoff Matrix can be helpful when developing profitable business strategies.

Click here for important legal disclaimers.