Credit note accounting: how does it work and what needs to be considered?

Issuing credit notes saves both buyers and sellers time and hassle, which is why it’s a popular form of billing. But how do you post a credit note? In accounting, the credit note must also appear on the balance sheet. What does the booking entry look like?

Credit note entries simply explained

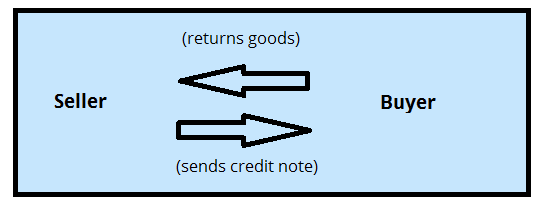

In another article, we explained what a credit note is. A credit note is also known as a credit memo, which is short for “credit memorandum.” It’s a document sent by a seller to the buyer, notifying them that a credit has been added to the customer’s account for goods returned. In this article, we will explain how to post credit notes correctly.

Making a credit note entry in the account

Credit notes are a little bit different to standard profit and loss posts, and therefore need to be entered differently. It also depends on whether you’re the buyer or the seller.

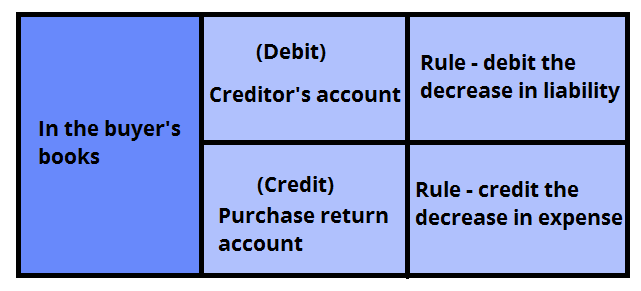

In the buyer’s account

Any goods returned by the buyer are regarded as purchase returns, which decreases the liability to pay the respective creditor and decreases the expense previously incurred to purchase said goods.

Creditor’s account | Debit |

To purchase return account | Credit |

If the buyer has not yet paid the seller, the credit note can be used to reduce the total liability. If the buyer has already paid the whole amount of the invoice, the buyer can decide whether they should use the credit note to offset any future payments to the seller, or as they can use it to demand a cash payment in exchange for the credit note.

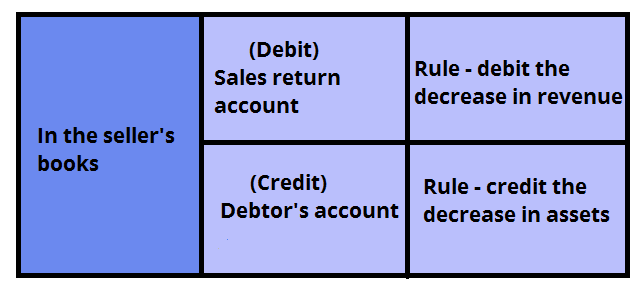

In the seller’s books

Goods returned to the seller are known as sales returns. By returning these goods to the seller, it results in a decrease in revenue previously booked as sales as well as a decrease in assets, since the debtor won’t be making the payment anymore.

Sales return account | Debit |

To debtor’s account | Credit |

The seller should always review any open credit notes they have at the end of each reporting period to see if they can be linked to open accounts receivable. This reduces the aggregate amount of invoices outstanding, and can be used to reduce payments to suppliers.

Please note the legal disclaimer relating to this article.

Related articles

Writing invoices: guidelines for businesses and the self-employed

Invoices are usually written with a special online tool or with an office software, like Microsoft Word or Excel. However, regardless of how you create an invoice, the content and structure of the document are subject to the same guidelines. But what do you need to be aware of? And what are the benefits of writing an invoice online?

Correcting or canceling an invoice

If you send many invoices per day, errors can often occur. This can then lead to issues with the tax office, and claiming back deductions owed to you. There are several options available to fix errors, however. In this article, we will show you how to create a correction and a cancellation invoice.

Booking company entertainment expenses

Most firms organize regular company events - business meals aren’t a rarity either. While selecting the menu plays an important role in the organization of such events, it’s just as important, if not more, to properly record all of your meal and entertainment expenses so that you can file for tax deductions.

How to correctly calculate, report, and reverse accruals on the balance sheet

Accruals play an important role when it comes to accounting. They are expenses or revenues incurred over a period in which no invoice was sent or no money changed hands. By learning more about accruals and how they work, you will be able to keep track of your company’s finances more easily. This article explains how to calculate, report, and reverse accruals in an easy-to-understand way.

How to book capital contributions and withdrawals correctly

If you want to use your company assets to strengthen company funds from your personal account, that isn’t a problem initially. However, you have to book these contributions and withdrawals correctly. It is important that these transactions do not affect the company’s profit or loss situation. Here’s what is important to make the right bookings.